A business loan through EMI is an essential source of finance for many companies, especially those that depend on quick credit, cash flow loans, and even business loan in Chennai. However, what if you forgot to pay your EMI in one single day?

Most entrepreneurs think a delay of one day is not a big deal. In fact, even for such a short delay banks will still penalize your account, flag it as a risky one for their credit departments and all of this will lead to a stressful situation for you. This article explains what to expect and how to control such occurrences in the future.

Practical Business EMI Handling Strategies: Loan for Business in Chennai

A business loan through EMI is an essential source of finance for many companies, especially those that depend on quick credit, cash flow loans, and even business loan in Chennai. However, what if you forgot to pay your EMI in one single day?

Most entrepreneurs think a delay of one day is not a big deal. In fact, even for such a short delay banks will still penalize your account, flag it as a risky one for their credit departments and all of this will lead to a stressful situation for you. This article explains what to expect and how to control such occurrences in the future.

1. Does a 1-Day EMI Delay Really Matter?

Yes, financially, at least. A single delay of one day does not classify your account as a risky one by the regulators, but still, lenders impose their internal rules.

Typically, the following events occur:

- There might be a late payment fee imposed on you.

- If auto-debit was used for the EMI and the debit failed, bounce charges might apply.

- Till the principal amount gets cleared, the penal interest for every day the amount remains unpaid might get accumulated.

- Automated reminders or follow-ups from the collections or Customer support team might be received.

Though the financial impact may be nearly insignificant for a day, otherwise the delay of non-payment even for a single day can be interpreted as poor repayment discipline and thus signify a lack of it.

2. Impact on Credit Score: Does a 1-Day Delay Affect It?

The positive side: Typically, a one-day delay in EMI does not lower your credit score. Credit bureaus such as CIBIL consider it a delinquency only when the payment is late for 30 days or more. Any delay of less than 30 days is generally not reported as a late payment on your report.

Nevertheless:

- Lenders maintain a record of past due occurrences for their internal records even if it is just one day.

- Short delays may influence lenders to perceive your risk profile as higher than what it is.

- During the processing of your future loan applications, they may look at your repayment history before making their decision.

Hence, your credit score may remain intact but your borrowing reputation is still affected.

3. Charges You Can Expect for a 1-Day Delay

In Chennai, various financial institutions have diverse ways of charging their customers, but the following are the most common fees:

a.Late Payment Fee

Normally, this charge is either a fixed amount or a small percentage of the monthly payment. Such fees may apply even for a single-day delay in EMI.

b.Bounce Charges

If you have opted for an EMI payment by NACH, ECS or cheque and it does not go through, the lender will charge a bounce fee along with your bank charging the same in some cases.

c.Penal Interest

This is interest charged per day on the overdue amount in addition to the regular interest. The daily interest is usually very small but still adds up to your total cost.

d.GST on Penalties

Many borrowers forget that GST increases the fees of some penalties, therefore the total amount payable increased.

Each of these charges is not very high individually, but for some businesses, the poor cash flows can cause these fees and charges to pile up over time.

4. How Lenders Track Late EMIs

Banks, non-banking financial companies (NBFCs), and every loan agency in Chennai have all turned to modern technology to keep an eye on repayments daily. Thus, even a 1-day delay brings about:

- Automated overdue alerts

- Regular reminders sent through SMS, WhatsApp, or email

- Internal records made of your payment conduct

- Follow-up on collection within 1–2 days

These four facts are part of the reason why they might never allow one short delay to go without counting you as a high-risk borrower even if no adverse report comes from an official credit bureau

5. Why Businesses in Chennai Commonly Face EMI Delays

Small and Medium Enterprises (SMEs) based in Chennai generally work within the sectors whose cash inflow and outflow vary on a daily basis like, for instance, trading, logistics, distribution, textiles, retail and manufacturing industries. The major causes of EMI blunders include:

- Delays in receiving payments

- Delays in cheques being cleared

- Weekends and bank holidays

- No sufficient funds in the EMI designated account

- Misconfigured auto-debit

- Simultaneous management of multiple loans

The one-day delay may appear to be trivial; however, during the times when cash flow is very tight, even the smallest bank delays can result in EMIs being overdue.

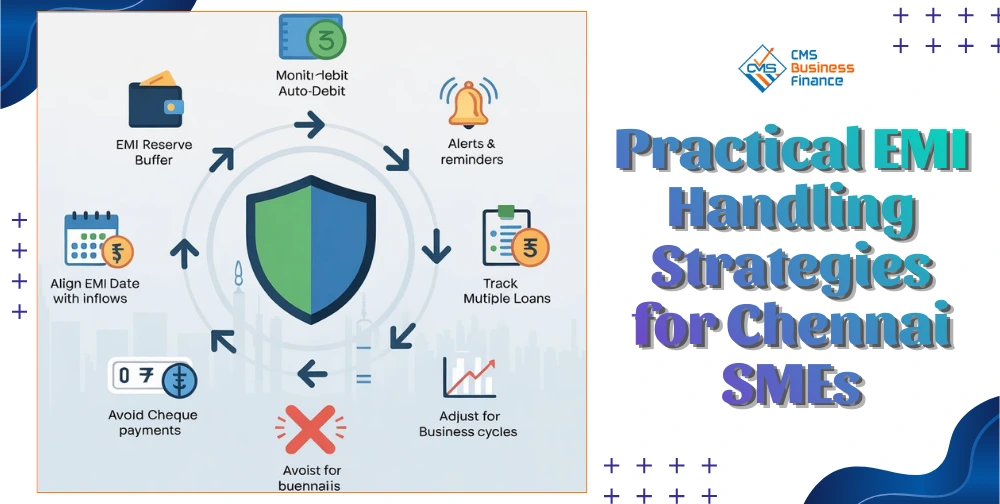

6. Practical Strategies to Avoid Accidental EMI Delays

a.Use Auto-Debit but Monitor It

Though ECS or NACH eliminates the possibility of manual oversights, it is still good practice to check your balance 48 hours prior to the due date.

b.Align EMI Dates with Incoming Payments

Select a due date right after the periods when you expect to receive the most payments.

c.Use Reminders and Alerts

Create alerts in your calendar, remind yourself through banking or app notifications.

d.Keep Track of Multiple Loans

If you handle more than one credit line, keep a simple spreadsheet with EMI dates and amounts updated.

e.Maintain an EMI Reserve Buffer

Keep at least 1 EMI amount should be kept in a separate account that is solely for loan payments.

f.Avoid Cheque-Based Payments for EMIs

Payments through cheques are likely to be delayed and they may have clearance issues, which may lead to the payment getting bounced and charged.

7. Business-Specific Tips for Chennai SMEs

- When your sales are subject to seasonality (e.g., wholesale, zari work, auto spares), insist on a rescheduling of EMI payments before you go into the peak/slow periods.

- For companies that deal with many suppliers and suffer from delayed customer payments, using a small overdraft facility may be their best bet for keeping an EMI safety net.

- Even if you pay a delayed EMI, do it as soon as possible, preferably within the same day. The sooner you pay, the less interest you will incur for the penalty.

Following these steps will not only prevent bigger issues in the future but also help if you have a loan for business in Chennai.

Conclusion: A 1-Day Delay Is Manageable—But Prevent It

The delay of just one day in EMI payment may not affect your credit score, but it comes at a price: late fees, penal charges, and internal risk flags. The financial penalty for a single delay may be insignificant but if you are a borrower who consistently pays late, your reliability will be affected.

- It is better to go for the preventive approach:

- Maintain an EMI buffer.

- Supervise auto-debits.

- Synchronize repayment dates with receivables.

- Simple systems for tracking dues.

These small habits can go a long way in helping businesses owners that are already dealing with fluctuating cash cycles to avoid unnecessary penalties and maintain their financial health in the long term.

Frequently Asked Questions

1️. Will a 1-day EMI delay on my business loan in Chennai affect my CIBIL score?

Ans: No. Credit bureaus generally consider delays only when EMIs are overdue for 30+ days. However, lenders still record the late payment internally, which may affect future borrowing.

- What charges can be applied if I miss my EMI by just one day?

Ans: You may face late payment fees, bounce charges (if auto-debit/cheque fails), penal interest on the overdue amount, and GST on penalties.

3️. How can I avoid accidental EMI delays for my business loan?

Ans: Maintain an EMI buffer amount, monitor auto-debits, align due dates with incoming payments, set reminders, and avoid cheque-based payments that may take time to clear.