Tack on high interest rates to over-borrowing and it becomes like an unending nightmare to manage. If you restrict yourself to under-borrowing, your company could actually end up having hard times. Emerging in 2026, the combination of high interest rates and stringent loan giving standards will not just make it a smart thing to know the exact amount of loan your company needs but also an essential thing for being able to survive.

The whole process of calculation is being periodically monitored, and you will get to know the proper way of borrowing an amount that is neither more nor less than required for a business loan in Chennai.

Why Exact Calculation Matters

Most of the time companies do not go bankrupt because they borrowed money, but they do so because they borrowed the wrong amount. Over-borrowing increases the EMI amount paid monthly which then reduces the profit. Under-borrowing leads to the need of emergency funding later on at very bad terms.

What is the solution then? There is a methodical way which is backed by your actual business figures.

Step 1: Analyse Your Cash Flow Gap

The first step is to determine the pattern of your monthly cash flows. For the next three months, record the following:

- Total sales revenue generated

- Total expenses incurred

- Any delay in timing between the two.

Example: A distributor in the wholesale market gets his payments after 1.5 months but he has to pay his suppliers in 15 days. If the monthly purchase is worth ₹800,000 and the company is making ₹1,000,000 monthly sales, then the working capital requirement for this gap of 30 days is ₹800,000.

Your calculation:

- Monthly revenue cycle (in days): _____

- Monthly expense cycle (in days): _____

- Gap period: _____

- Average monthly expenses: _____

- Working capital needed = (Average monthly expenses × Gap period) ÷ 30

Unsecured Business Loans in Chennai: Understanding Quick Capital Needs

When you have a need for cash that is not backed by assets, the unsecured business loans in Chennai are the quickest way to get cash. But they usually have a higher interest rate (which is estimated to be between 16% and 24% in 2026), thus making it even more vital to have accurate calculations done.

For unsecured funding, do not just calculate:

Immediate operational needs + 15% buffer = Unsecured loan amount

The 15% of the total amount borrowed is essentially for the time taken for processing and any unforeseen delays. Do not exaggerate this amount—each rupee that is borrowed amounts to a significant increase in the loan’s interest cost over time.

Real example: A firm engaged in digital marketing is in need of ₹5,00,000 for the purchase of new software and hiring of personnel. The amount arrived at after adding the 15% as buffer is ₹5,75,000, which is the exact amount you need to ask for.

Step 2: Calculate Growth Investment Requirements

If you are looking to expand, then you need to list down every single cost that you are going to incur:

Equipment/Assets:

- The price at which it will be purchased

- The amount for installation

- Trainer’s fee

- Amount to reserve for maintenance (first half a year)

Inventory:

- The worth of the initial stock

- Costs related to storage

- Insurance

Marketing/Setup:

- Expenses for the campaign

- Fees for hiring

- Costs for legal matters and registration

Add these up one after the other. Stay away from rounding numbers like “₹10 lakhs for expansion.” Instead, give figures such as “₹9,47,000 for expansion needs outlined in documents”.

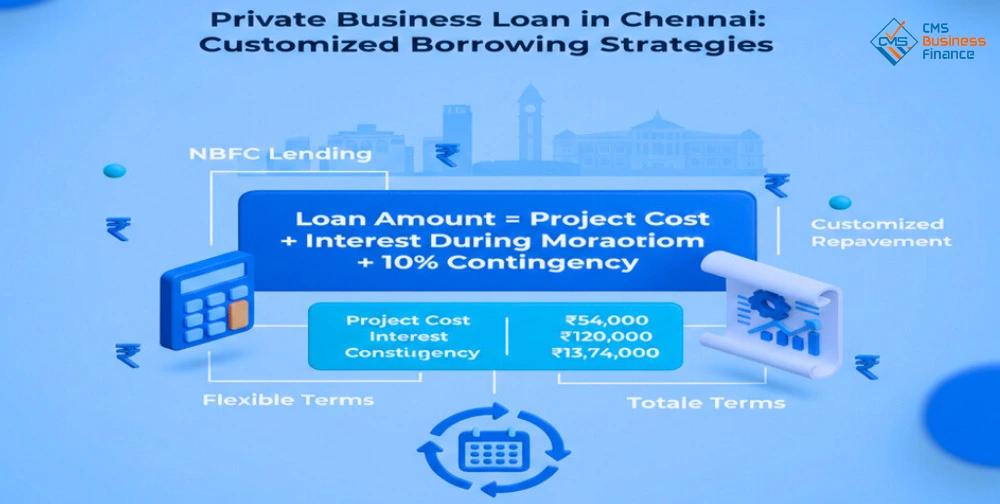

Private Business Loan in Chennai: Customized Borrowing Strategies

If a business needs flexible terms that are beyond what traditional banks offer, a private business loan in Chennai coming from Non-Banking Financial Companies and fintech lenders is the solution because they allow full customization. It is not unusual for these lenders to offer a repayment schedule that is aligned with the way your income patterns are.

The following formula should be used for private funding:

Loan Amount = Project Cost + Interest During Moratorium Period + 10% Contingency

Example: A restaurateur requires ₹12 lakhs for remodelling, expects a 3-month wait before the place opens, and accepts the offer of 18% annual interest from the lender.

- Cost of the project: ₹1200000

- Interest for 3 months: ₹12,00,000 × 18% × 3/12 = ₹54,000

- Contingency (10%): ₹1,20,000

- Exact total amount: ₹13,74,000

This reduces the possibility of running out of funds during the project.

Step 3: Check EMI Affordability

Your loan amount must fit within your repayment capacity. Use this critical formula:

a.Maximum EMI = (Monthly Profit × 40%) − Existing EMIs

Always make sure not more than 40% of your net monthly profit is used for loan installment payments. By doing so, you still have some room for making adjustments in your operations.

b.Calculate your maximum loan eligibility:

To illustrate, if the profit for the month is ₹2 lakhs and you owe nothing else:

- Maximum EMI you can afford: ₹80,000

- At 18% for 3 years, this lends support for a loan of around ₹22 lakhs

If your need as per the calculations is more than this amount, then either prolong the period, cut down the loan amount, or let your sales go up first before you decide to borrow.

Step 4: Add Strategic Buffer (Not Emotional Padding)

Once you have determined your exact requirements, you should add a strategic buffer:

- For working capital: 10-12%

- For purchasing equipment: 8-10%

- For expansion projects: 15-20%

The buffer relates to and incorporates real uncertainties such as changes in the supplier’s price or costs due to regulatory measures—no dreaming “extra cushion” thinking involved.

a.Final Calculation Template

Total Exact Loan Amount =

- Documented expense needs: _____

- Interest during deployment: _____

- Processing fees (1-3%): _____

- Strategic buffer (%): _____

- TOTAL: _____

Verify this total by means of your EMI affordability. If it doesn’t match, then extend the tenure or cut down the scope never go beyond your repayment capacity.

2026 Reality Check

In the current lending situation, accuracy indicates to lenders that the borrower is professional. The provision of thoroughly worked out calculations along with the necessary paperwork boosts the chances of approval and, alternatively, may lead to better interest rates being offered.

By collaborating with expert financial partners like CMSBusinessFinance, you will be able to improve your calculations and also find the right lending products that suit your particular business scenario.

Also, keep in mind: The amount of the loan that is best for you is not the maximum that you can get—rather, it is the minimum that you really need for the purpose of achieving your specific business goal.

Calculate with precision. Smart borrowing. Sustainable growth.

Frequently Asked Questions

- Why is it dangerous to guess the loan amount instead of calculating it?

Ans: Because businesses don’t fail due to borrowing money—they fail because they borrow the wrong amount.Over-borrowing increases EMI and kills profit, while under-borrowing forces expensive emergency funding later.

- What is the first thing a business must calculate before applying for a loan in 2026?

Ans: The cash flow gap.This includes understanding monthly revenue, expenses, and the timing difference between inflow and outflow.

- How do you calculate the working capital required for a cash flow gap?

Ans: Use – Working Capital = (Average Monthly Expenses × Gap Days) ÷ 30

This gives the exact amount needed to maintain operations without stress.