Private Finance vs Bank Loans in Chennai: Which Monthly Interest Option Works Better?

Gowri

Written By

Private Finance vs Bank Loans in Chennai: Which Is Better ?

If you need quick cash in Chennai, your choice between traditional bank loans and private lending is going to play a big role in your financial situation. Therefore, knowing the features of each of these lending options will help you make a wise choice that is not only affordable but also keeps you away from a debt trap.

Interest Rate Comparison: The Real Cost

|

Lender Type |

Interest Rate Range |

Monthly Interest |

Typical Loan Amount |

|

Public Sector Banks |

9.98% - 12% p.a. |

0.83% - 1% |

₹5 lakhs - ₹50 lakhs |

|

Private Banks |

10.5% - 14% p.a. |

0.87% - 1.17% |

₹3 lakhs - ₹40 lakhs |

|

NBFCs |

12% - 18% p.a. |

1% - 1.5% |

₹2 lakhs - ₹25 lakhs |

|

Private Lenders |

18% - 36% p.a. |

1.5% - 3% |

₹50,000 - ₹15 lakhs |

The interest rate is only one part of the calculation. What matters more is understanding whether your lender uses flat rate or reducing balance calculation methods.

The Critical Difference: Flat Rate vs Reducing Balance

A lot of the time, borrowers do not even realize that such a big difference exists between the two options. This one aspect could cost you multiple lakhs of rupees spread over the entire repayment period of the loan.

-

Flat Rate Interest: Flat Rate Interest: No matter how much you repay, interest on the entire amount will be calculated during the entire loan period. Thus, if you take a loan of ₹5 lakhs at 12% flat rate for 5 years, then you will pay ₹60,000 annually (₹5,000 monthly) which interest of ₹3 lakhs will be the total cost.

-

Reducing Balance Interest: Interest is calculated only on the outstanding principal and this principal amount reduces with each payment. The same loan of ₹5 lakhs at 12% reducing balance will approximately cost you the total interest of ₹1.67 lakhs, thus ₹1.33 lakhs will be the saving!

|

Loan Details |

Flat Rate (12%) |

Reducing Balance (12%) |

|

Principal Amount |

₹5,00,000 |

₹5,00,000 |

|

Loan Tenure |

5 years (60 months) |

5 years (60 months) |

|

Monthly EMI |

₹13,333 |

₹11,122 |

|

Total Interest Paid |

₹3,00,000 |

₹1,67,320 |

|

Total Repayment |

₹8,00,000 |

₹6,67,320 |

|

Your Savings |

— |

₹1,32,680 |

This comparison reveals why understanding your interest calculation method is non-negotiable when choosing between lending options.

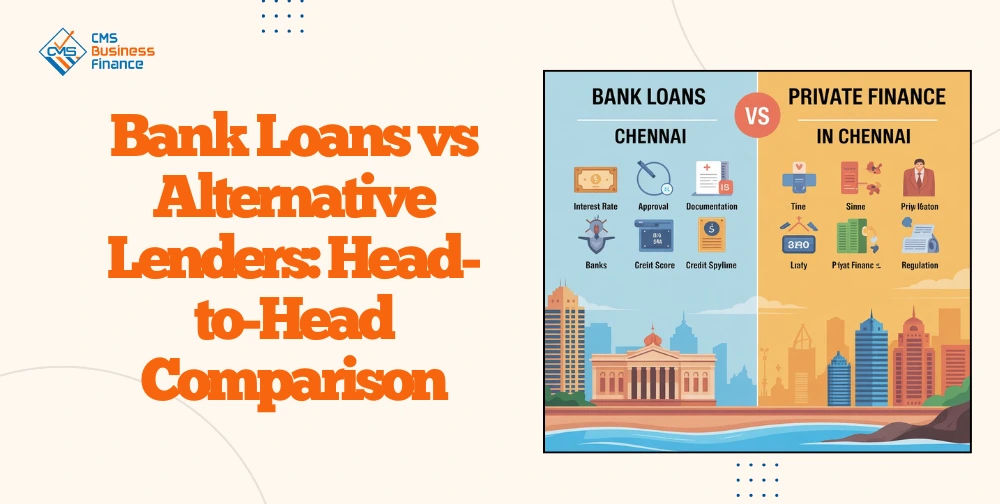

Bank Loans vs Alternative Lenders: Head-to-Head Comparison

|

Factor |

Bank Loans |

Alternative Lenders |

|

Approval Time |

5-14 days |

24-48 hours |

|

Credit Score Requirement |

700+ preferred |

600+ accepted |

|

Documentation |

Extensive (8-10 documents) |

Minimal (3-5 documents) |

|

Interest Calculation |

Reducing balance (standard) |

Often flat rate |

|

Regulation |

RBI-regulated |

Variable oversight |

|

Loan Tenure |

1-8 years |

6 months - 3 years |

|

Prepayment Penalty |

Usually none after 6 months |

Often 2-5% |

|

Best For |

Planned expenses, large amounts |

Emergencies, quick needs |

1.When Alternative Lending Makes Sense

Private finance in Chennai fulfils particular borrower requirements that banks are not able to meet. Take financing from alternative sources into account if you need money urgently for medical treatment that requires immediate hospitalization within 48 hours, need working capital for your business to take up a time-bound opportunity, have no or very poor credit rating leading to rejection of your application by the bank, or require money for unconventional use that is not fit for bank loan categories.

Reputable lenders such as CMSBusinessFinance are dedicated to thoroughly understanding the local business dynamics and provide tailored repayment plans that correspond to your cash flow cycle. Unlike inflexible bank schedules, these financial institutions support entrepreneurs, traders, and professionals to come up with a repayment schedule that is convenient for them and is thus, critical for the business community of Chennai.

2.The Smart Borrower's Strategy

Before you take out any loan, calculate the total repayment amount, not just the monthly interest. A lender with flat 2% monthly interest (i.e., 24% per annum) will cost you much more than another lender quoting 30% per annum on a reducing balance.

Example: ₹3 lakh loan for 2 years

-

2% monthly flat rate: Total interest = ₹1,44,000 (₹3,00,000 × 2% × 24 months)

-

30% p.a. reducing balance: Total interest = ₹1,02,000

Despite the higher advertised rate, the reducing balance method saves you ₹42,000!

Making the Right Choice for Your Situation

|

Your Situation |

Recommended Option |

Reason |

|

Good credit (750+), planned expense |

Bank loan |

Lowest cost, best terms |

|

Emergency medical need |

Alternative lender |

Speed critical, refinance later |

|

Credit score 600-700 |

NBFC or CMSBusinessFinance |

Balance of approval and cost |

|

Business working capital |

Alternative financing |

Flexibility, quick turnaround |

|

Debt consolidation |

Bank loan only |

Avoid compounding high interest |

|

Small amount (<₹1 lakh), short term |

Quick loan option |

Convenience outweighs cost |

The Chennai Advantage: Local Market Insights

Chennai's lending market is extremely competitive with different banks and other finance companies in places like T. Nagar, Anna Nagar, and Guindy competing quite intensely for the business of the clients. The competition is meant for you—banks and non-bank lenders will give you negotiable terms. Don't take the first offer—at least three lenders should be compared; they, along with competing quotes, shall be used to negotiate for better rates.

Local lenders know the city as far as its economic ups and downs are concerned. They even know when the textile trade is busiest, and real estate prices are at their highest and when there are payment delays in the IT sector. This type of local knowledge, for instance, CMSBusinessFinance, results in giving more realistic repayment schedules based on your actual cash flow rather than sticking you to inflexible monthly commitments.

Actionable Steps: Your 72-Hour Loan Strategy

Hour 0-24: Review your credit score through CIBIL or Experian, if you can. Work out precisely how much money you need—ask for a loan of just that amount. Get the basic documents together: Aadhaar, PAN, last 3 months' bank statements.

Hour 24-48: If your credit is good and you have time, apply at 2-3 banks at once. For urgent cases or poorly rated credit, contact a lender who is registered and get a quick assessment. Get a letter with quotes that show total repayment, not just monthly interest, and ask for it.

Hour 48-72: Turn out total costs from all options and compare them. Inquire about the interest calculation method. Go through the agreement very carefully paying attention especially to prepayment terms and default penalties. Only after you are fully clear about all the terms, proceed to sign.

The Bottom Line

When you are looking for a private loan in Chennai, the first thing you need to do is to understand the actual cost apart from the advertised monthly rates. Alternative lending has a crucial role in the financial ecosystem of the city, as it offers the speed and flexibility that the traditional banks are unable to provide. But this ease of access comes with a higher price.

The loan cost should be your main point to consider. Then compare at least three different offers and choose one based on your particular needs instead of the advertised monthly interest rate. If you go for the bank route or the alternative lender, always calculate the total repayment amount in rupees, check the lender's credentials, and ensure that the monthly EMI is comfortably within your budget. Your financial future hinges on this one decision—make it a great one. We hope this blog provides you with a clear insight into bank and private loan options. Check the options based on your needs and choose wisely. This blog highlights key factors from our analysis. Ensure you fully understand the loan process before you apply.