Step-by-Step EMI Calculation Guide

GOWRI

Written By

How to Calculate EMI for a Business Loan in Chennai

Business operations require financial resources which force most business owners to use loans as their primary funding method to expand their companies. The essential inquiry to address before entering into any contractual agreement in any business loan in chennai requires you to determine whether your business possesses sufficient funds to make EMI payments.

The ability to assess EMI payments enables businesses to maintain their cash flow while safeguarding their financial resources. The guide provides a step-by-step process to calculate financial metrics which banks and NBFCs use for their operations in India.

What Is an EMI?

EMI (Equated Monthly Instalment) is the fixed amount you repay to a lender every month until the loan is fully paid off. The total payment amount for the loan period consists of two parts which include the main loan amount and the interest portion that needs to be paid back.

The standard formula used by all financial institutions is:

EMI = P × r × (1 + r)^n / ((1 + r)^n − 1)

(this formula is copyrighted from emicalculator.global/)

The formula defines these components

-

P = Principal loan amount

-

r = Monthly interest rate (for annual rate calculation ÷ 12 ÷ 100)

-

n = Loan tenure in months

Example: For a ₹10 lakh loan at 14% annual interest over 36 months, the monthly rate r = 14/12/100 = 0.01167. The EMI works out to approximately ₹34,178.

How Interest Rates Affect Your EMI

The monthly outflow of your payments will change when the annual interest rate difference reaches 1 to 2 percent. The loan costs more because higher interest rates increase both the monthly payment and the total interest amount that will be paid throughout the entire loan period.

The banks and NBFCs charge interest rates between 12% and 24% per annum for business loans in Chennai based on the applicant's credit profile and business experience and their revenue stability. The effective annual rate (EAR) should be used for comparison purposes because it reveals actual borrowing costs, which extend beyond the nominal rate that lenders present.

How Tenure Affects Total Repayment

The longer loan term results in reduced monthly payments, but it increases total loan expenses. The shorter loan term requires higher monthly payments, yet it results in lower total expenses throughout the loan period.

People need to choose their loan term because it determines the amount they can afford to pay each month and their total borrowing expenses. A business with strong, predictable monthly revenue may prefer a shorter tenure to reduce interest outgo. A business with seasonal or irregular income may need a longer tenure to keep monthly obligations manageable.

How to Evaluate EMI Affordability When Choosing Business Loan Providers in Chennai

The process of evaluating business loan providers in Chennai requires more than interest rate comparisons to identify suitable terms from public sector banks and private banks and NBFCs. The assessment process requires you to review the processing fees together with the prepayment penalties and the repayment options which should be evaluated together with the EMI amount. The platform CMS Business Finance provides businesses with tools to compare lenders while they learn about the actual borrowing costs before selecting a lender.

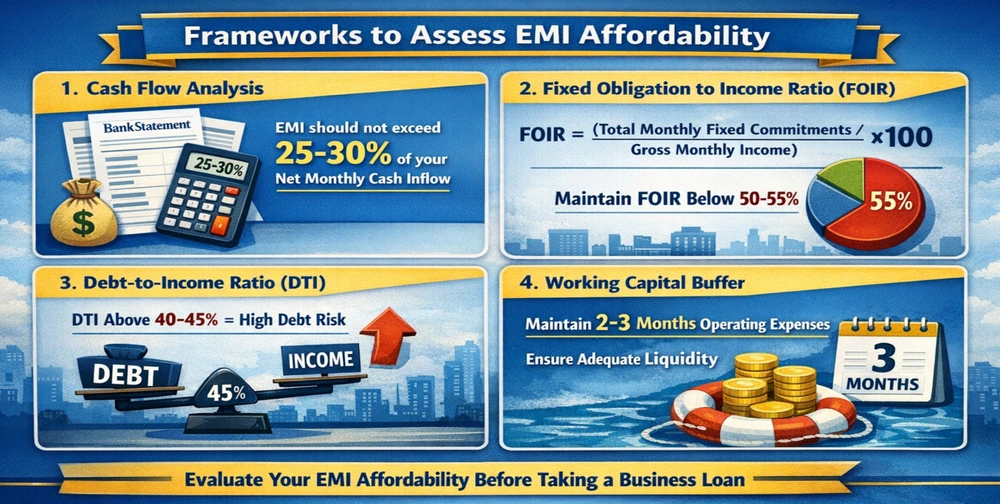

Frameworks to Assess EMI Affordability

1. Cash Flow Analysis

Examine your bank statements from the previous year. Determine your monthly income after deducting necessary business expenses. The business should use surplus cash to pay the EMI because essential business costs need to remain intact.

A standard rule: the EMI should not exceed 25–30% of your average monthly net cash inflow.

2. Fixed Obligation to Income Ratio (FOIR)

FOIR calculates the ratio of all fixed monthly debt payments to total monthly income.

FOIR = (Total Monthly Fixed commitments ÷ Gross Monthly Income) × 100

(this formula is copyrighted from investingmultiple.com)

Most banks in India require business loan applicants to maintain a FOIR which should remain below 50 to 55 percent. Your existing EMIs I need to calculate your new loan EMI which will result in unsafe borrowing limits.

3. Debt-to-Income Ratio (DTI)

The DTI metric applies to all debt obligations through its calculation of debt repayments against income similar to the FOIR system. A DTI above 40 to 45 percent indicates that a business possesses excessive debt which makes it difficult to handle revenue decreases.

4. Working Capital Buffer

After paying the EMI, does your business retain enough liquid funds to cover 2–3 months of operating expenses? The buffer exists to allow businesses to manage payment delays and seasonal downturns and sudden expenses that arise unexpectedly. The loan requires a reassessment of its size and duration when the EMI results in complete depletion of working capital.

Key Financial Red Flags and APR Checks in a Private Business Loan in Chennai

NBFCs and fintech lenders offering private business loan in Chennai often deliver loan money faster than traditional banks yet their interest rates remain higher. When evaluating such offers, verify the APR (Annual Percentage Rate) which includes all fees — not just the stated interest rate — before calculating your actual EMI burden.

Common Financial Red Flags When Borrowing

Before you sign a loan agreement, please pay attention to these alert signals which show potential problems ahead:

-

If EMI surpasses 30% of net monthly cash flow, there may be repayment stress.

-

No cash flow projection was completed; borrowing money without projecting future income is very risky.

-

Relying on future credit to pay off present debt is a structural red flag.

-

Ignoring total repayment cost — focus only on low EMI, not total interest paid

-

Overestimating revenue when determining affordability, use cautious, realistic income estimates.

Conclusion

A single step task exists to determine whether a person can afford to pay their loan EMI. The process demands full assessment of your cash flow situation and ongoing financial responsibilities and your upcoming needs for working capital and expected revenue stream.

The EMI formula calculates monthly payments while the FOIR and DTI frameworks show your current debt level. Business revenue which fluctuates will turn an EMI which appears affordable into financial difficulty.

Businesses should borrow responsibly by selecting amounts their operations can handle and choosing loan durations which balance their fiscal responsibilities with their financial obligations.